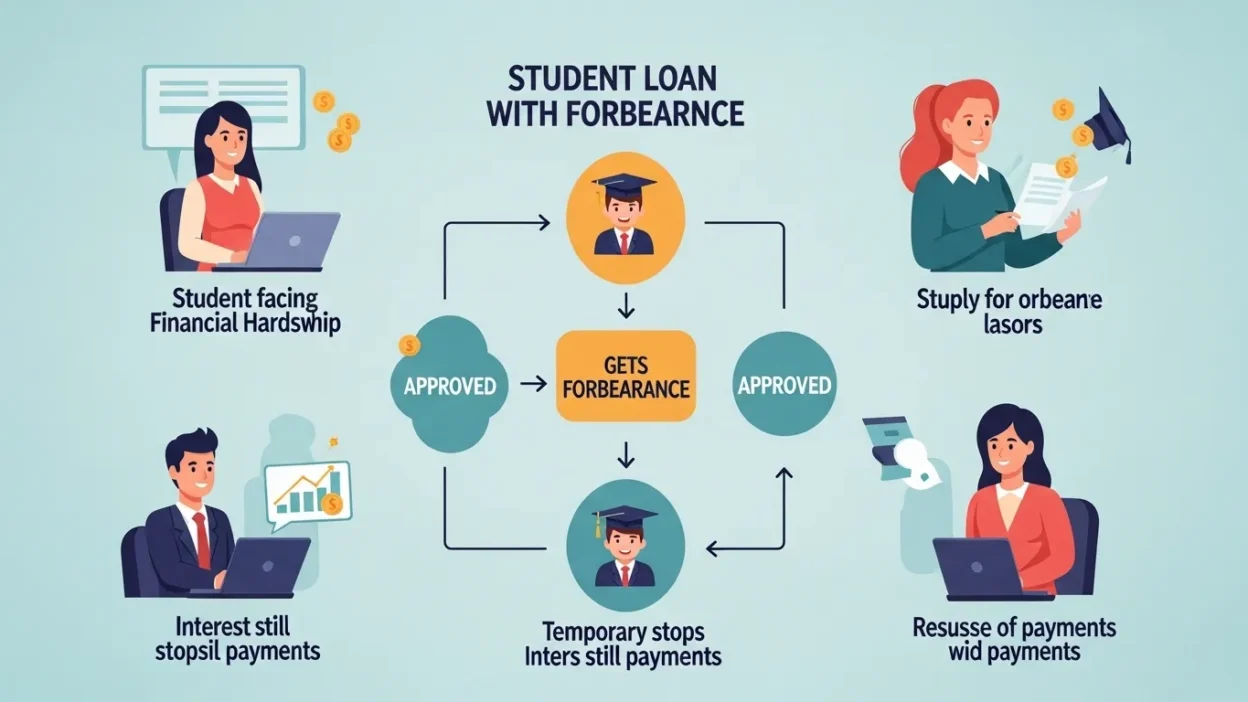

Paying off student loans can be overwhelming, especially when unexpected financial challenges arise. For many borrowers, keeping up with monthly payments is not always feasible, which is where student loan forbearance comes in.

Simply put, forbearance allows you to temporarily pause or reduce your loan payments when you face financial hardship, medical emergencies, or other qualifying situations.

While it provides immediate relief, it’s important to understand that interest often continues to accrue, which can increase your total loan balance over time.

In this comprehensive guide, we’ll break down the meaning of student loan forbearance, explain how it works, and explore the different types available. You’ll also learn about its advantages and disadvantages, how it differs from deferment, and when it might be the right choice for you.

By the end, you’ll have a clear understanding of how forbearance can help you manage your student loans responsibly without jeopardizing your financial future.

What Is Forbearance in Student Loans?

Student loan forbearance is a temporary relief option that allows borrowers to pause or reduce their loan payments when they face financial difficulties. Unlike loan forgiveness, which cancels some or all of your debt, forbearance is only a short-term solution to help you manage payments without falling into default. It is commonly used by borrowers who experience unexpected expenses, temporary unemployment, or medical emergencies.

When you enter forbearance, your loan servicer grants you a period during which you may either stop making payments entirely or pay a reduced amount, depending on the type of forbearance and your eligibility. Most federal student loans allow forbearance in increments of up to 12 months, and the total time you can use forbearance is typically capped at 36 months over the life of the loan.

One crucial point to understand is that interest continues to accrue during forbearance for most loans, including both federal and private student loans. If unpaid, this interest may be capitalized—added to your principal balance—making your overall debt larger once regular payments resume.

Forbearance is not a permanent fix but rather a tool to prevent default and give borrowers breathing room during difficult times. Knowing how it works and when to use it can help you manage your loans responsibly while avoiding unnecessary financial stress.

How Student Loan Forbearance Works

Student loan forbearance provides borrowers with a temporary break from making full payments on their loans. The process begins when a borrower contacts their loan servicer to request forbearance, explaining their financial hardship or the reason they need relief. Approval is typically based on eligibility criteria and the type of loan, and in many cases, the servicer can grant forbearance without extensive documentation for federal loans.

Once approved, you can either pause your payments entirely or make reduced payments for a set period, usually up to 12 months at a time. Many borrowers renew forbearance if they continue to face financial challenges, but most federal loans have a maximum cumulative limit of 36 months over the life of the loan.

It’s important to note that interest continues to accrue during forbearance for most federal and private loans. For unsubsidized federal loans and most private loans, this accrued interest may later be capitalized, increasing the total amount you owe once regular payments resume.

Forbearance is often easier to qualify for than deferment, making it a popular choice for borrowers who need immediate, short-term relief. However, while it can prevent late payments and default, it does not reduce your principal or eliminate interest. Therefore, it’s most effective when used strategically during temporary financial hardships, rather than as a long-term solution for managing debt.

Types of Student Loan Forbearance

Student loan forbearance comes in two main types: general (or discretionary) forbearance and mandatory forbearance. Understanding the differences can help borrowers choose the option that best fits their situation.

General (Discretionary) Forbearance

General forbearance is granted at the discretion of the loan servicer. Borrowers must request it and provide a reason for needing relief. Common situations include financial hardship, temporary unemployment, medical expenses, or unexpected life events. While it is often easier to obtain than deferment, approval is not guaranteed, and the servicer evaluates each request individually. Interest continues to accrue on all loans during general forbearance, which can increase the total balance over time.

Mandatory Forbearance

Mandatory forbearance is required by law for borrowers who meet specific eligibility criteria. If you qualify, your loan servicer must approve your request. Typical qualifying situations include:

- Serving in the National Guard or military

- Working in public service or as a teacher eligible for forgiveness programs

- Participating in medical or dental residency programs

- Having high student loan debt relative to income

Mandatory forbearance ensures that borrowers in certain circumstances receive protection without being denied. Like general forbearance, interest continues to accrue, so unpaid interest may be added to the principal balance once regular payments resume.

By knowing the type of forbearance you qualify for, you can make informed decisions, avoid default, and manage your student loans effectively during periods of financial difficulty.

Does Interest Accrue During Student Loan Forbearance?

One of the most important aspects of student loan forbearance is understanding how interest behaves while your payments are paused. For most federal and private student loans, interest continues to accrue during the forbearance period. This means that even though you are not making full payments, your loan balance may grow over time.

For subsidized federal loans, the government temporarily covers the interest during periods like deferment, but in forbearance, interest generally accrues on all loan types, including subsidized loans if you choose forbearance. Unsubsidized loans and private loans always accrue interest during forbearance, which can significantly increase the total amount you owe over time.

This accrued interest may later be capitalized, meaning it is added to your principal balance. Capitalization increases the total debt and can lead to higher monthly payments once regular repayment resumes. For example, if you have a $10,000 loan with a 5% interest rate and you pause payments for one year, roughly $500 of interest could be added to your balance if unpaid.

Because of this, it is often recommended, when possible, to make interest-only payments during forbearance. Doing so prevents your loan balance from growing and reduces the long-term cost of your student loans.

Understanding how interest accrues helps borrowers make informed decisions, ensuring that forbearance is used strategically as a short-term solution rather than a long-term way to avoid payments.

Forbearance vs Deferment: What’s the Difference?

While both forbearance and deferment offer temporary relief from student loan payments, they are not the same, and understanding the differences can help you choose the best option for your situation.

Forbearance

Forbearance allows borrowers to pause or reduce payments temporarily due to financial hardship, medical emergencies, or other qualifying reasons. The key point is that interest continues to accrue on nearly all loans during forbearance, including federal and private loans. Unpaid interest may later be capitalized, increasing the overall loan balance. Forbearance is often easier to qualify for than deferment, making it a popular option for short-term financial difficulties.

Deferment

Deferment is a similar payment pause, but it is generally reserved for specific situations, such as returning to school, unemployment, economic hardship, or active military duty. One significant advantage of deferment is that interest may not accrue on certain subsidized federal loans during the deferment period. This can make deferment more cost-effective than forbearance in cases where borrowers qualify.

Key Differences

| Feature | Forbearance | Deferment |

|---|---|---|

| Eligibility | Discretionary / temporary hardship | Specific qualifying situations |

| Interest accrual | Usually yes | Often no for subsidized loans |

| Approval | Easier to get | Must meet strict criteria |

| Impact on loan balance | May increase due to capitalization | Less likely if interest is subsidized |

Choosing between forbearance and deferment depends on your eligibility, financial situation, and long-term repayment goals. Understanding these differences ensures you use the option that minimizes costs while protecting your credit.

Who Qualifies for Student Loan Forbearance?

Student loan forbearance is designed to help borrowers who are temporarily unable to make full payments due to financial or personal challenges. Both federal and some private loan borrowers may be eligible, but the exact criteria depend on the loan type and the loan servicer’s requirements.

For general (discretionary) forbearance, borrowers typically need to demonstrate financial hardship. This can include:

- Temporary unemployment or underemployment

- Unexpected medical expenses

- Emergency family situations

- Other short-term financial difficulties

Borrowers request this type of forbearance directly from their loan servicer, and approval is at the servicer’s discretion. While easier to obtain than deferment, it is not guaranteed.

Mandatory forbearance, on the other hand, is available to borrowers who meet specific eligibility requirements, and loan servicers must grant it if the borrower qualifies. Common qualifying circumstances include:

- Serving in the National Guard or military

- Participating in medical or dental residencies

- Being employed in public service or teaching positions eligible for loan forgiveness

- Having high student loan debt relative to income

Both types of forbearance allow temporary relief, but interest continues to accrue, so borrowers should weigh the benefits against potential increases in the total loan balance.

Understanding who qualifies ensures that borrowers can access temporary relief responsibly, avoid default, and manage their student loans effectively while navigating short-term financial challenges.

Pros and Cons of Student Loan Forbearance

Student loan forbearance can be a valuable tool for borrowers facing temporary financial difficulties, but it also comes with potential drawbacks. Understanding the advantages and disadvantages helps borrowers use it wisely.

Pros of Forbearance

- Temporary Payment Relief – Forbearance allows you to pause or reduce payments during financial hardship, helping prevent missed payments or default.

- Avoid Late Fees and Collections – By using forbearance, borrowers can protect their credit scores and avoid late fees that come with missed payments.

- Easier to Qualify For – Compared to deferment, forbearance generally has fewer eligibility requirements, making it accessible for more borrowers.

- Short-Term Solution – It provides immediate relief during temporary financial challenges such as job loss, medical emergencies, or unexpected expenses.

Cons of Forbearance

- Interest Accrual – Interest continues to accumulate on most loans, including federal and private loans. If unpaid, it may be capitalized, increasing your principal and total repayment amount.

- Longer Repayment Period – Using forbearance can extend the life of your loan, as accrued interest adds to the balance.

- Higher Total Loan Cost – Because of capitalization, borrowers may end up paying significantly more over the life of the loan.

- Not a Permanent Fix – Forbearance only provides temporary relief and does not reduce or forgive debt.

Overall, forbearance is most effective when used strategically for short-term relief. Borrowers should weigh the immediate benefits against the long-term cost, and consider alternatives like income-driven repayment plans or deferment if those options better suit their situation.

When Should You Use Student Loan Forbearance?

Student loan forbearance can be a helpful tool, but it’s important to use it strategically to avoid long-term financial consequences. Forbearance is best suited for temporary financial difficulties rather than long-term repayment challenges.

Situations Where Forbearance Makes Sense

- Short-Term Financial Hardship – If you are temporarily unemployed, underemployed, or facing unexpected expenses, forbearance can give you a break from payments until your income stabilizes.

- Medical Emergencies – Large medical bills or health-related challenges can make it difficult to stay current on loans. Forbearance allows you to focus on recovery without worrying about default.

- Temporary Job Loss – If you are in between jobs, forbearance provides time to secure new employment while preventing late payments.

- Natural Disasters or National Emergencies – During crises, such as natural disasters or economic downturns, forbearance may be offered automatically by federal loan servicers to affected borrowers.

Situations Where Forbearance May Not Be Ideal

- If you can manage reduced payments under an income-driven repayment plan, this may be a better option to avoid interest capitalization.

- For long-term financial struggles, repeatedly using forbearance can increase your overall loan balance significantly.

- If you are close to qualifying for loan forgiveness programs, accumulating extra interest could reduce the benefit.

Using forbearance wisely means evaluating your current financial situation, the length of relief needed, and the potential interest costs. It is most effective as a short-term solution to prevent default and protect your credit while giving you time to regain financial stability.

How to Apply for Student Loan Forbearance

Applying for student loan forbearance is a straightforward process, but it requires careful preparation to ensure your request is approved. The steps differ slightly between federal and private loans, but the overall process is similar.

Step 1: Contact Your Loan Servicer

The first step is to reach out to your loan servicer—the company that manages your student loan payments. Explain your financial situation and your need for temporary relief. Your servicer can provide the necessary forms and guide you through the application process.

Step 2: Determine Eligibility

You will need to show that you qualify for either general or mandatory forbearance. For general forbearance, you may need to provide evidence of financial hardship, such as recent pay stubs, unemployment documentation, or medical bills. Mandatory forbearance is granted automatically if you meet specific criteria, such as serving in the military or working in qualifying public service jobs.

Step 3: Submit Your Request

Complete and submit the forbearance request form provided by your servicer. Make sure to include all required documentation to avoid delays.

Step 4: Receive Confirmation

Once your request is reviewed, your loan servicer will notify you whether it has been approved. If approved, your payments may be paused or reduced, and you will receive details on the duration of your forbearance.

Step 5: Monitor Your Loan

Even during forbearance, interest may accrue. Keep track of your loan balance and consider making interest-only payments if possible to prevent your balance from growing.

Applying for forbearance proactively ensures you avoid late payments and protect your credit, while giving you temporary financial relief.

Alternatives to Student Loan Forbearance

While forbearance can provide short-term relief, it is not always the most cost-effective solution due to interest accrual and potential loan balance growth. Fortunately, there are several alternatives that borrowers may consider to manage student loans without increasing long-term debt.

1. Income-Driven Repayment Plans

Federal borrowers can apply for income-driven repayment (IDR) plans, which adjust monthly payments based on income and family size. Payments can be as low as $0 per month if your income is very low, and interest may be partially subsidized depending on the plan. Unlike forbearance, these plans keep your loan in active repayment, preventing interest capitalization on subsidized loans.

2. Loan Deferment

Deferment allows borrowers to temporarily pause payments, similar to forbearance, but interest may not accrue on subsidized federal loans. Deferment is often ideal for students returning to school, those experiencing economic hardship, or military service members.

3. Loan Consolidation or Refinancing

Consolidation combines multiple federal loans into a single loan with a fixed interest rate, potentially lowering monthly payments. Private refinancing can reduce interest rates, but may require good credit and stable income.

4. Loan Forgiveness Programs

Public Service Loan Forgiveness, Teacher Loan Forgiveness, and other federal programs can cancel part or all of your student loans if you meet specific employment requirements. These programs are often better long-term solutions than repeated forbearance.

By exploring alternatives, borrowers can maintain repayment progress, minimize interest accrual, and reduce the total cost of their loans, making these options potentially more advantageous than forbearance in many situations.

How Forbearance Affects Your Credit Score

Many borrowers worry about the impact of student loan forbearance on their credit score. The good news is that approved forbearance generally does not negatively affect your credit. When your loan servicer grants forbearance, your account remains in good standing, and payments are considered temporarily suspended, not missed.

Key Points to Consider:

- No Negative Reporting – As long as your forbearance request is approved, your servicer will report your account as current to the credit bureaus. This means your credit score should not drop due to entering forbearance.

- Avoiding Default – Forbearance can protect borrowers from delinquency or default, both of which have severe negative effects on credit scores and can remain on your report for up to seven years.

- Interest Accrual – While credit is not directly affected, the interest that accrues during forbearance can increase your total loan balance. If you do not plan for repayment carefully, higher balances may affect debt-to-income ratios, which can indirectly impact your ability to qualify for new credit.

- Private Loans – Forbearance policies vary for private lenders. Most reputable private lenders report approved forbearance as current, but it is always a good idea to confirm with your loan servicer.

In short, student loan forbearance, when approved, is a safe tool to protect your credit while managing temporary financial difficulties. The main consideration is the long-term cost due to accrued interest, rather than immediate credit impact.

How Forbearance Affects Long-Term Loan Costs

While student loan forbearance can provide temporary relief, it often comes with long-term financial consequences. The primary factor affecting costs is interest accrual. During forbearance, interest continues to accumulate on most federal and private loans. If left unpaid, this interest may be capitalized, meaning it is added to your principal balance. As a result, your total loan balance grows, leading to higher monthly payments once repayment resumes.

For example, consider a $15,000 loan with a 5% interest rate. If you pause payments for one year without paying interest, approximately $750 in interest could be added to your principal. This means you would owe $15,750 when regular payments restart. Over time, continued forbearance or multiple periods of paused payments can significantly increase the overall repayment amount, sometimes by thousands of dollars.

In addition to increased balances, forbearance can extend your repayment timeline. Longer repayment periods result in more interest paid over the life of the loan, even if monthly payments are manageable.

Borrowers can mitigate these long-term costs by making interest-only payments during forbearance, which prevents interest from being capitalized. Understanding the financial impact of forbearance ensures that borrowers use it strategically, as a short-term tool rather than a long-term solution.

Ultimately, forbearance is a temporary safety net, but borrowers should carefully weigh the benefits of short-term relief against the potential increased cost of their student loans over time.

Tips for Managing Student Loans During Forbearance

Entering student loan forbearance can provide much-needed relief, but it’s important to manage your loans carefully to minimize long-term costs and avoid financial surprises. Here are some practical tips to help you navigate this period effectively.

1. Monitor Your Loan Balance

Even though payments are paused, interest continues to accrue. Regularly check your loan statements to track how much interest is accumulating. This helps you plan for repayment once forbearance ends.

2. Make Interest-Only Payments if Possible

Paying just the interest during forbearance prevents it from capitalizing—that is, being added to your principal balance. Even small payments can save hundreds or thousands of dollars over the life of your loan.

3. Stay in Communication with Your Loan Servicer

Keep your loan servicer updated on any changes in your financial situation. If your hardship continues, you may be able to extend forbearance or explore alternatives like income-driven repayment plans.

4. Prepare for the End of Forbearance

Set aside funds or adjust your budget so you can resume regular payments without stress. Understanding the new payment amount—including accrued interest—prevents missed payments and late fees.

5. Explore Alternatives

Before or during forbearance, review other options such as deferment, income-driven repayment, or loan forgiveness programs, which may reduce long-term costs more effectively.

By proactively managing your loans during forbearance, you can use this temporary relief strategically, protect your credit, and minimize the impact on your overall student loan debt.

Common Mistakes Borrowers Make with Forbearance

While student loan forbearance can be a helpful tool, many borrowers make mistakes that increase their overall debt or reduce the effectiveness of this temporary relief. Being aware of these pitfalls can help you avoid unnecessary financial strain.

1. Using Forbearance Too Frequently

Some borrowers rely on forbearance repeatedly instead of exploring other repayment options. Frequent pauses can significantly increase your total loan balance due to interest accrual and capitalization. For long-term financial stability, it’s better to consider income-driven repayment plans or other alternatives for repeated financial difficulties.

2. Ignoring Accrued Interest

Interest continues to accumulate during forbearance for most loans. Ignoring it can lead to unexpected increases in your principal balance, which makes future payments higher. Making interest-only payments during forbearance can prevent this issue.

3. Not Exploring Alternatives

Borrowers sometimes jump straight to forbearance without considering options like deferment, refinancing, or income-driven repayment plans, which may be more cost-effective and reduce long-term interest.

4. Waiting Too Long to Request Forbearance

Delaying the forbearance request until after missing payments can negatively impact your credit. It’s crucial to contact your loan servicer before missing payments to ensure your account remains in good standing.

5. Misunderstanding Eligibility and Terms

Not fully understanding the type of forbearance you qualify for, its duration, and whether interest accrues can lead to financial surprises. Always review your loan servicer’s guidelines carefully.

Avoiding these common mistakes ensures that forbearance serves its purpose as a temporary, strategic solution rather than a long-term financial burden.

(FAQs)

Many borrowers have questions about how student loan forbearance works, its effects, and whether it’s the right choice. Here are answers to some of the most common questions.

1. How long can student loan forbearance last?

For most federal loans, forbearance is granted for up to 12 months at a time, with a maximum cumulative period of 36 months over the life of the loan. Private loans may have different limits, depending on the lender.

2. Does forbearance affect your credit score?

Approved forbearance does not negatively impact your credit score. Payments are considered temporarily paused, and your account remains in good standing.

3. Can private student loans go into forbearance?

Some private lenders offer forbearance, but policies vary widely. Always check with your loan servicer for eligibility, documentation requirements, and interest policies.

4. Does interest accrue during forbearance?

Yes, for most federal and private loans, interest continues to accrue. Unpaid interest may be capitalized, increasing the total loan balance. Making interest-only payments can help reduce long-term costs.

5. Is forbearance the same as loan forgiveness?

No. Forbearance only pauses or reduces payments temporarily. Loan forgiveness cancels some or all of your debt permanently, typically under special programs like Public Service Loan Forgiveness.

6. Can I make payments during forbearance?

Yes. You can choose to make full or partial payments, especially interest-only payments, to prevent your loan balance from growing while still receiving temporary relief.

Understanding these common questions helps borrowers use forbearance strategically, avoid unnecessary costs, and manage their student loans responsibly.

Conclusion:

Student loan forbearance can be a lifesaving option for borrowers facing temporary financial hardship.

By allowing you to pause or reduce your payments, it helps prevent missed payments, late fees, and potential loan default, protecting both your credit score and financial stability.

However, forbearance is a short-term solution, not a permanent fix.

One of the most important considerations is interest accrual. For most loans, interest continues to build during forbearance, and unpaid interest may be capitalized, increasing the total loan balance and future monthly payments.

Because of this, borrowers should carefully weigh the benefits of temporary relief against the long-term cost. Whenever possible, making interest-only payments during forbearance can help mitigate these effects.

Forbearance works best when used strategically for example, during short-term unemployment, medical emergencies, or other temporary financial challenges.

Borrowers should also explore alternatives, such as income-driven repayment plans, deferment, loan refinancing, or forgiveness programs, which may provide more cost-effective solutions for managing loans.

Ultimately, understanding how forbearance works, who qualifies, and its financial implications allows borrowers to make informed decisions.

When used responsibly, forbearance provides a valuable safety net, giving you the breathing room needed to regain financial footing while keeping your student loans on track.

By approaching forbearance thoughtfully, you can navigate temporary difficulties without jeopardizing your long-term financial health and remain in control of your student loan journey.