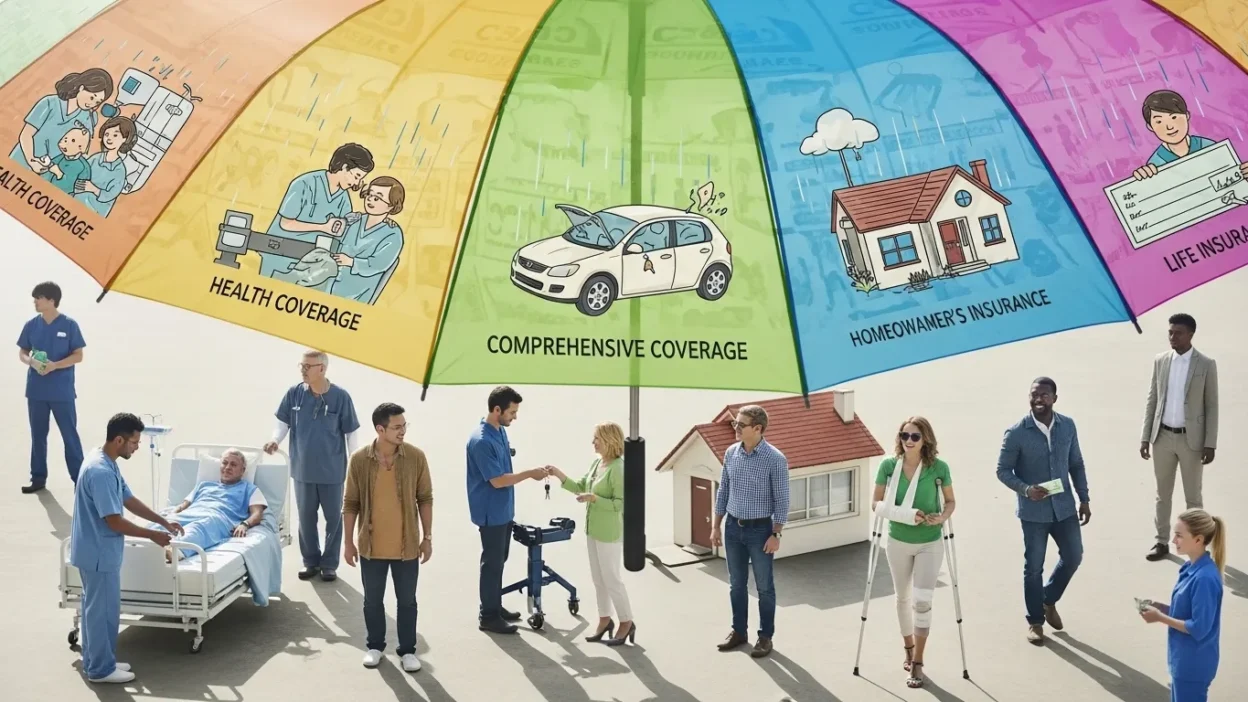

When you hear the term comprehensive coverage, you might immediately think of insurance. While it is commonly used in the insurance industry, the phrase actually applies to many areas, including journalism, healthcare, service plans, and even education.

At its core, comprehensive coverage means complete, thorough, and inclusive protection or reporting, covering multiple aspects rather than just one part. In insurance, for example, it goes beyond accidents to include theft, natural disasters, and vandalism.

In news reporting, it ensures all angles of a story are addressed, providing readers with a full understanding. Understanding what comprehensive coverage really means is important because it helps you make informed decisions, whether you are choosing an insurance plan, evaluating a service, or assessing information.

In this article, we’ll explore the meaning, examples, advantages, and practical applications of comprehensive coverage, helping you grasp the concept fully and use it effectively in real life.

What Does Comprehensive Coverage Mean?

The term comprehensive coverage combines two simple words comprehensive and coverage but together they convey a powerful concept. Comprehensive means complete, thorough, or all-encompassing, while coverage refers to protection, reporting, or the extent to which something is included. Put together, comprehensive coverage refers to broad, detailed, and inclusive protection or reporting, ensuring that most, if not all, important aspects are addressed.

In practical terms, comprehensive coverage means that nothing important is overlooked. For instance, in insurance, it protects you from risks beyond standard incidents, such as theft, fire, natural disasters, or vandalism. In media, comprehensive coverage ensures that news stories are reported from multiple angles, including background information, different perspectives, and detailed facts. In service plans, it means including a wide range of features, benefits, or support, leaving little room for gaps.

The key characteristic of comprehensive coverage is its all-inclusive nature. Unlike partial or limited coverage, it is designed to minimize exposure to risks or information gaps. However, it is also important to understand that “comprehensive” does not always mean everything is covered exclusions or limitations may still exist.

By understanding this concept, you can make informed choices when selecting insurance policies, evaluating services, or assessing news sources. Comprehensive coverage isn’t just a term it’s a standard of thoroughness and reliability that ensures peace of mind and complete protection in many areas of life.

Comprehensive Coverage in Insurance

In the world of insurance, the term comprehensive coverage is most often associated with auto insurance, but it also applies to health, home, and other types of policies. Essentially, it refers to protection that goes beyond standard coverage, safeguarding against a wide range of risks that are not caused by collisions or accidents.

For example, comprehensive auto insurance typically covers:

- Theft – protection if your vehicle is stolen.

- Vandalism – damages caused intentionally by others.

- Natural disasters – floods, storms, hail, or falling trees.

- Fire – damage from accidental fires.

- Animal-related damage – collisions with animals like deer.

Unlike collision coverage, which specifically addresses damages from accidents with other vehicles, comprehensive coverage is designed to protect against unexpected or non-collision events. It gives car owners peace of mind, knowing that many unpredictable scenarios are accounted for.

However, it’s important to note that comprehensive coverage does not cover everything. Typical exclusions include wear-and-tear, mechanical breakdowns, or intentional damage caused by the owner. Additionally, deductibles and policy limits can affect the payout in the event of a claim.

Choosing comprehensive coverage is a balance between cost and protection. While premiums are higher than basic insurance, the wide-ranging protection can save you from substantial financial loss. For many vehicle owners, comprehensive coverage provides complete peace of mind, making it a crucial part of any well-rounded insurance plan.

Comprehensive Coverage in Media and Journalism

In journalism, the term comprehensive coverage takes on a slightly different meaning. Instead of insurance protection, it refers to reporting that is complete, balanced, and thorough, ensuring that audiences receive a full understanding of an event or issue. Comprehensive coverage in media is not just about reporting the facts; it involves context, multiple perspectives, and continuous updates.

For instance, when a major political event occurs, a media outlet providing comprehensive coverage will include:

- Background information – explaining the history or causes leading up to the event.

- Multiple viewpoints – featuring opinions from different stakeholders, experts, or affected communities.

- Detailed facts – verifying statements, providing statistics, and reporting verified outcomes.

- Ongoing updates – following developments as the situation evolves.

This type of reporting allows audiences to form well-informed opinions and reduces the risk of misinformation. In contrast, partial or limited coverage might only report the headline or one perspective, leaving readers with an incomplete picture.

Comprehensive coverage is particularly important in today’s fast-paced digital world, where news spreads quickly and misinformation can take root. Audiences rely on thorough reporting to make sense of complex events, whether in politics, disasters, science, or social issues.

Ultimately, comprehensive coverage in media is about trust, reliability, and depth. Just as comprehensive insurance protects against unforeseen risks, comprehensive journalism protects the public against misinformation by providing a complete and accurate portrayal of reality.

Comprehensive Coverage in Health and Service Plans

In healthcare and service industries, comprehensive coverage refers to a plan or policy that includes a wide range of benefits and services, designed to meet most or all of an individual’s needs. Unlike basic or limited plans, which cover only essential services, comprehensive plans aim to minimize gaps in care or protection, offering broader security and convenience.

In health insurance, comprehensive coverage often includes:

- Doctor visits – primary care and specialist consultations

- Hospitalization – inpatient care and surgical procedures

- Prescription medications – coverage for essential medicines

- Preventive care – screenings, vaccinations, and wellness programs

- Emergency services – ambulance, urgent care, and trauma treatment

Similarly, in service plans such as electronics warranties, home protection plans, or subscription services comprehensive coverage ensures that a variety of potential problems or needs are addressed. For example, a comprehensive home warranty may cover plumbing, electrical systems, heating, and major appliances, rather than just one or two items.

While comprehensive plans usually cost more than basic alternatives, the benefits often outweigh the extra expense, particularly for individuals or families seeking peace of mind. However, it is important to review the terms carefully, as comprehensive coverage may still include exclusions, limits, or deductibles.

Ultimately, comprehensive health or service plans are about protection, reliability, and convenience, ensuring that policyholders are prepared for a wide range of eventualities, whether planned or unexpected.

Key Characteristics of Comprehensive Coverage

Comprehensive coverage, whether in insurance, media, health, or services, has several defining characteristics that set it apart from partial or limited protection. Understanding these features helps individuals and organizations assess whether a policy, plan, or service truly meets their needs.

1. Broad Scope

A primary feature of comprehensive coverage is its wide-ranging scope. It aims to include multiple risks, events, or aspects rather than focusing on a single area. For example, comprehensive auto insurance protects against theft, fire, natural disasters, and vandalism, not just collisions. Similarly, a comprehensive news report includes background information, multiple viewpoints, and ongoing updates.

2. All-Inclusive Protection

Comprehensive coverage seeks to minimize gaps in protection or reporting. This all-inclusive approach ensures that most foreseeable scenarios are accounted for, providing peace of mind and reducing the risk of unexpected losses.

3. Detailed and Thorough

Another hallmark is thoroughness. Comprehensive coverage goes beyond surface-level or minimal inclusion. In health plans, this means covering both preventive and emergency care. In services, it involves addressing all relevant components, rather than just the obvious ones.

4. Higher Cost but Greater Security

While comprehensive coverage often comes with higher premiums or fees, the trade-off is broader protection and reduced risk. For many, the added cost is justified by the security, reliability, and convenience it provides.

In essence, comprehensive coverage is defined by its breadth, depth, and reliability. By prioritizing thoroughness over minimalism, it ensures that users are protected, informed, or supported across multiple dimensions.

Comprehensive Coverage vs Other Types of Coverage

Understanding comprehensive coverage is easier when we compare it with other types of coverage, such as collision, liability, or basic insurance. Each type serves a different purpose, and the differences can help you choose the right plan for your needs.

Comprehensive vs. Collision Coverage

While comprehensive coverage protects against non-collision events like theft, fire, vandalism, or natural disasters, collision coverage focuses specifically on damage resulting from vehicle collisions. For example, if a car hits a tree, collision coverage applies, but if a tree falls on the car during a storm, comprehensive coverage is needed. Many car owners combine both for full protection.

Comprehensive vs. Liability Coverage

Liability coverage is designed to protect you against damage or injury caused to others, not your own property. Comprehensive coverage, on the other hand, protects your property from unexpected events. While liability is often mandatory, comprehensive coverage is usually optional but highly recommended for broader security.

Comprehensive vs. Basic or Standard Coverage

Basic coverage offers minimal protection, typically covering only essential risks. Comprehensive coverage is broader and more inclusive, addressing multiple scenarios and reducing gaps. While basic coverage is cheaper, it may leave policyholders exposed to unexpected costs.

In summary, comprehensive coverage stands out for its breadth and inclusiveness, while other types of coverage are narrower in scope. Understanding these differences helps individuals and businesses make informed decisions about which policies provide the most reliable protection for their unique needs.

Advantages of Comprehensive Coverage

Comprehensive coverage offers several benefits that make it a preferred choice in insurance, healthcare, media, and service plans. While it may come with a higher cost compared to basic or limited coverage, the advantages often outweigh the expense, providing security, convenience, and peace of mind.

1. Broad Protection

One of the main advantages is wide-ranging protection. Comprehensive coverage safeguards against multiple risks or includes multiple aspects of a service, reducing the chances of unexpected gaps. For example, in auto insurance, it covers theft, natural disasters, vandalism, and more, not just collisions.

2. Peace of Mind

Knowing that many potential risks are covered provides emotional reassurance. Individuals and families can rest easy, knowing they are prepared for unforeseen events, whether it’s a medical emergency, vehicle damage, or home repairs.

3. Financial Security

Comprehensive coverage can prevent significant financial loss. By including multiple scenarios or services, it reduces the likelihood of large out-of-pocket expenses for events that would otherwise be uncovered.

4. Reliability and Convenience

Comprehensive coverage often comes with additional services and support, making it easier to navigate complex processes like filing insurance claims or receiving timely medical care.

5. Thoroughness Across Contexts

Whether in media reporting, health plans, or service agreements, comprehensive coverage ensures complete and detailed inclusion, helping users make informed decisions and reducing uncertainty.

Overall, comprehensive coverage is not just about protection; it is about preparing for the unexpected, reducing risk, and ensuring reliability in a variety of real-world situations.

Disadvantages of Comprehensive Coverage

While comprehensive coverage offers broad protection and peace of mind, it is not without drawbacks. Understanding the potential disadvantages helps individuals make informed decisions about whether the benefits justify the costs.

1. Higher Cost

The most obvious downside of comprehensive coverage is the higher premiums or fees. Because it includes protection against a wide range of risks or services, the cost is typically more than basic or limited coverage. For some individuals or families, this added expense may not be justified if they rarely encounter the covered scenarios.

2. Possible Overcoverage

Comprehensive coverage can sometimes lead to paying for protections or services you may never use. For example, a car owner may pay for coverage against theft in an area with very low crime rates, resulting in unnecessary expense.

3. Deductibles and Policy Limits

Even with comprehensive coverage, policies often include deductibles, limits, or exclusions. This means that some incidents may still require out-of-pocket payment, and not all risks are fully covered. Misunderstanding these terms can lead to frustration during claims.

4. Complexity

Comprehensive plans can be more complex to understand, with detailed terms, clauses, and conditions. Policyholders may need to spend more time reviewing and comparing options to ensure they get the protection they need.

5. False Sense of Security

Finally, some people may assume “comprehensive” means everything is covered, leading to potential surprises if certain events fall outside the policy.

In conclusion, while comprehensive coverage is highly valuable, it comes with higher costs, complexity, and potential overcoverage, which should be weighed carefully against individual needs and circumstances.

Who Needs Comprehensive Coverage

Comprehensive coverage is not necessary for everyone, but for certain individuals and situations, it provides valuable protection and peace of mind. Understanding who benefits most can help you decide whether the added cost is worth it.

1. Vehicle Owners in High-Risk Areas

Car owners living in areas prone to theft, vandalism, or natural disasters benefit greatly from comprehensive auto insurance. It protects against a wide range of non-collision events, such as storm damage, fire, or falling objects, reducing the risk of unexpected financial loss.

2. Families with Health Concerns

For families with existing medical conditions or high healthcare needs, comprehensive health insurance ensures coverage for doctor visits, hospitalization, preventive care, and prescriptions. This can help minimize out-of-pocket expenses while providing consistent access to care.

3. Homeowners or Renters

Homeowners and renters benefit from comprehensive coverage in property or service plans, which may cover plumbing, electrical systems, appliances, or accidental damage. This helps protect valuable assets and reduces repair costs in the event of unexpected incidents.

4. Individuals Seeking Peace of Mind

Even without high-risk circumstances, comprehensive coverage is suitable for people who prefer broad protection and reliability. It reduces uncertainty by providing inclusive coverage across multiple scenarios.

5. Businesses and Organizations

Companies that own property, vehicles, or equipment can use comprehensive coverage to protect against financial losses from a wide range of risks, ensuring continuity and security.

In summary, comprehensive coverage is most valuable for those who face multiple risks, want thorough protection, or seek peace of mind. By assessing your needs and circumstances, you can determine if this all-encompassing coverage is the right choice for you.

How to Choose the Right Comprehensive Coverage

Selecting the right comprehensive coverage requires careful evaluation to ensure you get maximum protection without overspending. Here are key steps to help you make an informed decision.

1. Assess Your Needs

Start by identifying the areas where you require protection. For car owners, consider risks such as theft, natural disasters, and vandalism. For health insurance, evaluate medical history, family needs, and potential treatments. Understanding your specific needs will help you choose a plan that is both practical and cost-effective.

2. Compare Plans and Policies

Not all comprehensive coverage plans are the same. Take time to compare different policies, looking at what they include and exclude. Check whether the coverage addresses the risks that matter most to you, and avoid paying for unnecessary extras.

3. Review Exclusions and Limits

Even comprehensive coverage may have exclusions, limitations, or deductibles. Carefully review the policy to understand what is and isn’t covered, as well as the maximum payout amounts. This helps prevent surprises during a claim.

4. Evaluate Deductibles and Premiums

Balance the premium cost with the deductible. A lower premium may come with a higher deductible, which could affect your out-of-pocket expenses. Choose a combination that fits your budget while still providing adequate protection.

5. Read Customer Reviews and Seek Advice

Look for real-world feedback from other policyholders to gauge the reliability and customer service of the provider. Consulting with an insurance agent, financial advisor, or expert can also provide valuable guidance.

By following these steps, you can select comprehensive coverage that meets your unique needs, providing peace of mind, thorough protection, and financial security.

Common Misunderstandings About Comprehensive Coverage

Despite its widespread use, many people misinterpret what comprehensive coverage actually includes. Understanding common misconceptions can help you make better decisions and avoid surprises.

1. “Comprehensive Means Everything is Covered”

A common myth is that comprehensive coverage guarantees protection against all possible risks. In reality, policies always have exclusions and limits. For example, a car insurance policy may not cover mechanical breakdowns or wear-and-tear, and health plans may exclude certain elective procedures.

2. Confusing Comprehensive with Full Coverage

People often assume comprehensive coverage is the same as “full coverage,” but the two are not identical. Full coverage usually refers to a combination of comprehensive and collision insurance, plus liability protection, whereas comprehensive alone covers non-collision events only.

3. “Higher Cost Always Equals Better Coverage”

While comprehensive plans tend to be more expensive, higher premiums do not automatically mean better protection. It is important to review the policy details, including deductibles, limits, and exclusions, to ensure it meets your needs.

4. Overlooking Fine Print

Many misunderstandings arise because policyholders don’t read the fine print. Comprehensive coverage may include conditions, restrictions, or requirements such as timely reporting of claims that affect payouts.

5. Assuming All Risks Are Equal

Some people believe that all included risks are equally relevant. However, depending on your location, lifestyle, or circumstances, certain protections may be more important than others.

By being aware of these misconceptions, you can use comprehensive coverage effectively, avoiding gaps, unnecessary costs, and disappointment when filing claims or seeking services.

Real-Life Examples of Comprehensive Coverage

Understanding comprehensive coverage becomes much easier when you look at real-life scenarios across different contexts. These examples illustrate how it provides protection, reliability, and peace of mind.

1. Auto Insurance

Imagine a car parked on the street during a storm. A falling tree branch damages the windshield and hood. With comprehensive auto insurance, the vehicle owner is covered for the repair costs. If the same car were stolen, the policy would also cover the loss. Without comprehensive coverage, the owner would need to pay out-of-pocket for these non-collision events.

2. Health Insurance

A family subscribes to a comprehensive health plan. One member requires surgery while another needs routine preventive care, including vaccinations and annual checkups. The plan covers both events, ensuring financial security and access to necessary care. In contrast, a basic plan might cover only emergencies or hospitalizations, leaving gaps for preventive treatments.

3. Media and Journalism

During a natural disaster, a news outlet providing comprehensive coverage reports not only on immediate damages but also on background causes, government responses, and community impact. Audiences receive a complete picture, rather than just isolated updates.

4. Service Plans

A homeowner purchases a comprehensive home warranty. When the plumbing system malfunctions and a major appliance breaks down simultaneously, both repairs are covered under a single plan. This avoids multiple service contracts and reduces stress and costs.

These examples demonstrate that comprehensive coverage is about preparing for multiple eventualities, offering broad protection, and ensuring that individuals, families, or organizations are not caught unprepared when unexpected events occur.

Frequently Asked Questions (FAQs) About Comprehensive Coverage

Comprehensive coverage can be complex, and many people have questions about how it works in different contexts. Here are some of the most common FAQs to help clarify the concept.

1. What is the simple meaning of comprehensive coverage?

Comprehensive coverage means broad, thorough, and inclusive protection or reporting. It covers multiple aspects of an event, service, or risk, rather than just one specific area.

2. Is comprehensive coverage the same as full coverage?

No. Full coverage usually combines comprehensive, collision, and liability insurance in one plan. Comprehensive alone protects against non-collision events, like theft, fire, or natural disasters.

3. What does comprehensive coverage not include?

Even comprehensive plans have exclusions. Common items not covered include wear-and-tear, mechanical failures, intentional damage, or elective procedures depending on the policy. Always check the fine print.

4. Is comprehensive coverage worth it?

For many, yes. While premiums may be higher, the protection against multiple risks and peace of mind make it valuable for car owners, families, homeowners, and businesses seeking reliable coverage.

5. How do I choose the right comprehensive coverage?

Start by assessing your needs, comparing plans, checking exclusions, evaluating premiums and deductibles, and reading customer reviews. Consulting with experts or advisors can also ensure you select the best option.

By answering these common questions, individuals and families can better understand comprehensive coverage and make informed decisions about which policies or plans meet their unique needs.

Conclusion

Comprehensive coverage is a term that carries significant importance across multiple areas, from insurance and health plans to media reporting and service agreements.

At its core, it refers to complete, inclusive, and thorough protection or reporting, ensuring that most relevant aspects are addressed rather than leaving gaps.

In insurance, it safeguards against non-collision events such as theft, fire, vandalism, or natural disasters, providing financial security and peace of mind. In health and service plans, it ensures access to a broad range of benefits, from preventive care to emergency services.

In journalism, comprehensive coverage ensures readers or viewers receive full, balanced, and reliable information.

While comprehensive coverage often comes with higher costs and complex terms, its advantages such as broad protection, reduced risk, and reliability typically outweigh the disadvantages for those who face multiple risks or desire thorough coverage.

Understanding the limitations, exclusions, and fine print is essential to avoid misunderstandings and make informed decisions.

Ultimately, whether you are selecting an insurance policy, evaluating a health plan, or relying on information sources, comprehensive coverage is about preparation, reliability, and complete protection.

By recognizing its value and applying it appropriately, you can make choices that provide security, reduce uncertainty, and help you navigate unexpected situations confidently.

Comprehensive coverage is not just a term it is a standard for ensuring thoroughness, safety, and peace of mind in the complex world of modern risks and services.

Welcome to TextFlirtz.com, your ultimate destination for flirty, fun, and clever text messages! Whether you’re looking to break the ice, charm your crush, or keep the sparks alive in your relationship, we’ve got a treasure trove of pick-up lines, flirty texts, and witty messages that make flirting effortless and exciting. Dive in, explore, and let your words do the magic—because at TextFlirtz.com, every message is a chance to flirt smarter, not harder.